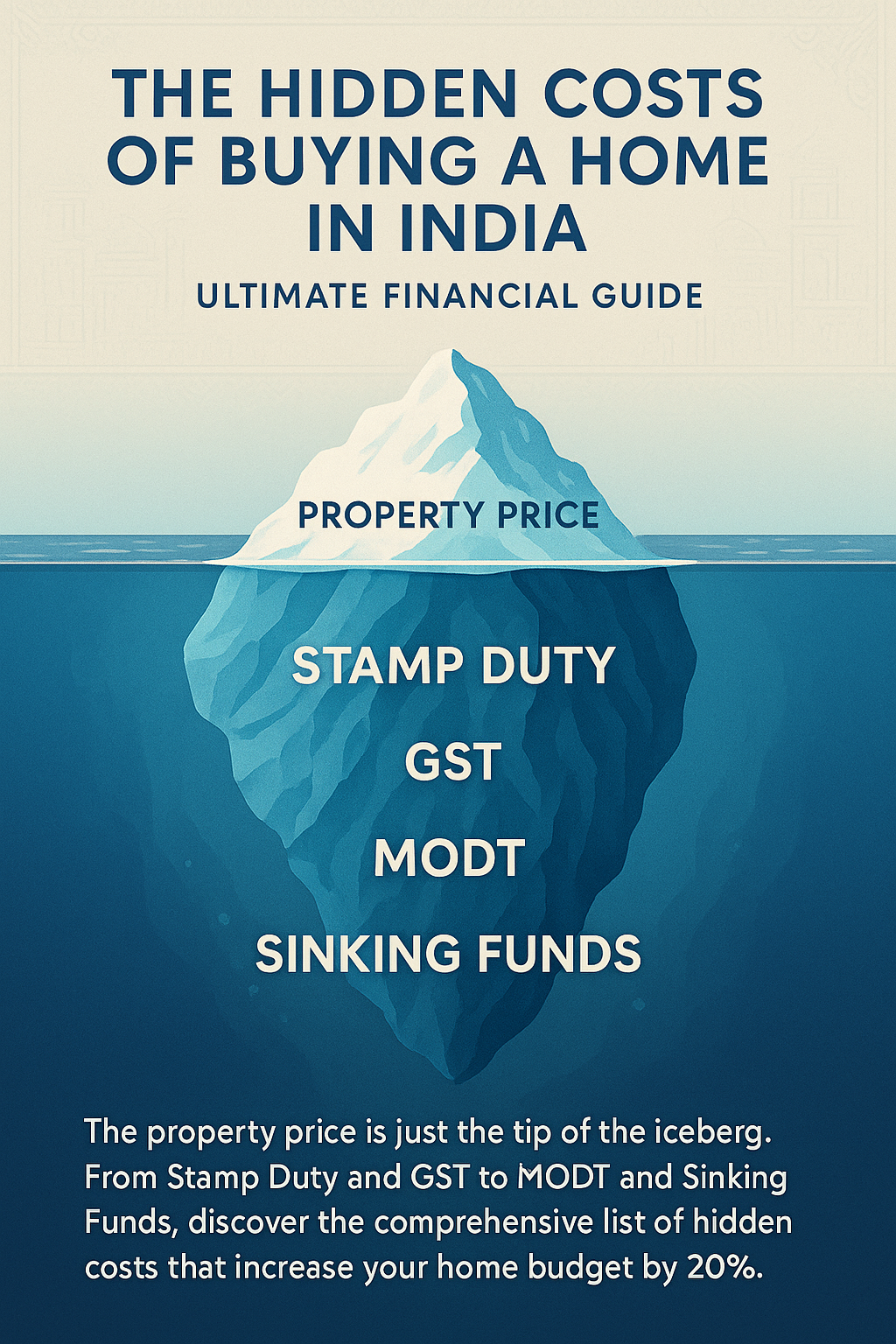

The Price Tag is a Lie: The Comprehensive Guide to Hidden Costs in Indian Real Estate

Imagine this scenario: You have spent months scouring property portals. You finally find the perfect apartment listed for a standard market price. You do the mental math—you have your down payment saved (usually 20%), and your bank has pre-approved a loan for the remainder. You think you are ready to sign the deal.

Stop right there.

If you walk into a builder's office or a seller's negotiation with only the "Base Price" or "Agreement Value" in mind, you are heading for a severe financial crisis. In the Indian real estate market, the advertised price is never the final price. It is merely the starting point of a much more expensive conversation.

Between government statutorily mandated taxes, banking technicalities, builder-imposed infrastructure fees, and the sheer cost of making a concrete shell habitable, the final "Cost of Acquisition" is typically 20% to 25% higher than the base price. For a standard mid-range home, that means you need to arrange lakhs in additional funds—money that usually cannot be funded by a home loan.

This guide acts as your financial flashlight, illuminating every dark corner where hidden costs lurk, ensuring your dream home doesn't become a budgeting nightmare regardless of when you buy.

1. Statutory Costs: The Government’s Share

These are mandatory levies imposed by the State and Central governments. They are non-negotiable, and failing to budget for them is the most common reason deals fall through at the last minute.

A. Stamp Duty (The Biggest Hit)

Stamp Duty is a tax you pay to the state government to legally validate your purchase documents. Without paying this, your sale deed has no legal standing in a court of law. It is the single largest "hidden" cost you will face.

- The Cost: It varies significantly by state and is subject to periodic revision, but typically ranges from 5% to 7% of the property's market value (or Circle Rate, whichever is higher).

- The Financial Impact: On a high-value property, this is a massive sum. Crucially, banks generally do not include Stamp Duty in the home loan amount. You must pay this out of your own pocket before the registration date.

- Gender Concession: Many states offer a 1% to 2% rebate if the property is registered in a woman's name (either as a sole owner or joint owner). This can result in significant savings, making it financially wise to consider registering the property in the name of a female family member.

B. Registration Charges

While Stamp Duty pays for the tax, Registration Charges pay for the administrative act of recording the deed in the local sub-registrar’s books to prove ownership.

- The Cost: This is usually 1% of the property value or a fixed cap, depending on the specific state laws at the time of purchase.

- Why it matters: While it seems small compared to Stamp Duty, on high-value transactions, even 1% is a significant amount of liquidity to arrange instantly.

C. Goods and Services Tax (GST)

This is often the most confusing aspect for modern buyers. GST applies only to properties that are Under-Construction.

- Standard Rate: Typically 5% of the property value for standard housing (without Input Tax Credit).

- Affordable Housing: A reduced rate of 1% usually applies to homes that fall under the "affordable" definition (based on carpet area and price caps defined by the government).

- Ready-to-Move Exemption: 0% GST. If the builder has received the Completion Certificate (CC) or Occupation Certificate (OC), legally, the transaction is treated as a sale of a completed immovable property, and no GST is applicable. This often makes ready-to-move flats financially attractive despite their higher base rates.

D. TDS on Property Purchase

If the property value exceeds a certain threshold (currently ₹50 Lakhs), the buyer is legally required to deduct 1% TDS (Tax Deducted at Source) from the payment made to the seller and deposit it with the Income Tax Department.

- The Trap: While this theoretically comes out of the seller's money, it is the buyer's responsibility to do the paperwork (Form 26QB). If you forget to deduct or deposit this, you are liable to pay the penalty and interest to the tax department, not the seller.

2. Builder & Society Charges: The "Infrastructure" Loading

When buying in a gated community or a new project, the "Base Price" usually covers only the apartment itself. The lifestyle amenities—which are likely why you chose the project—come with their own substantial price tags.

A. Preferred Location Charges (PLC)

Do you want a flat on a higher floor for the breeze? Or one facing the swimming pool? In real estate, every view has a price.

- Floor Rise Charges: Builders often charge an extra per-square-foot rate for every floor you go up. By the time you reach the higher floors (15th or 20th), this "floor rise" premium can add a significant amount to the per-square-foot base rate.

- View Charges: Pool-facing, garden-facing, or main-road-facing units often carry a premium of 5% to 10% of the base cost. This is entirely discretionary and set by the builder.

B. Car Parking Space

In most metropolitan cities, buying a car park is mandatory and separate from the flat cost. You cannot simply park in the compound; you must own the slot.

- The Cost: Depending on whether it is an open spot, a covered (stilt) spot, or a mechanized puzzle stack, prices can range from a few lakhs to very high premiums for multiple spots. Some luxury projects treat parking slots as premium real estate in themselves.

C. Advance Maintenance Deposit

Builders need cash flow to maintain the society (security, cleaning, lifts, gardening) until the Resident Welfare Association (RWA) is formed and takes over. They often collect maintenance charges for a long duration upfront.

- The Calculation: Builders typically ask for 12 to 24 months of maintenance in advance. If the monthly maintenance is calculated on a per-square-foot basis, this results in a large lump sum due on the day of possession.

D. Sinking Fund / Corpus Fund

This is a "safety net" fund collected to handle future heavy capital expenditures (like repainting the building in 5 years, waterproofing, or replacing a broken lift).

- The Cost: This is usually a substantial lump sum or calculated as a multiple of the monthly maintenance. While this money is eventually transferred to the society's bank account, it is an immediate cash outflow for you at the time of possession and is non-negotiable.

E. Club House & Utility Fees

Builders often charge a one-time "Club House Development Fee" and separate fees for installing essential infrastructure.

- The Cost: You may see charges for "Meter Installation," "Water Connection," "Piped Gas Infrastructure," or "Sewerage Treatment Plan." These "utility" bundles are often grouped together and can amount to several lakhs. Never assume electricity and water connections are included in the base price.

3. Loan-Related "Technical" Charges

You might think, "The bank is charging me interest, so everything else should be free." Unfortunately, banks have several administrative costs that are passed on to the borrower.

A. Processing Fee

The fee to process your application and run credit checks. * The Cost: typically a percentage of the loan amount plus applicable taxes. * Negotiation Tip: This is the easiest fee to get waived. Always ask for a waiver, especially during festive seasons or month-ends when banks are chasing targets.

B. MODT / MOE Charges

The Memorandum of Deposit of Title Deed (MODT) constitutes a legal undertaking that you have deposited the property papers with the bank as security. The state government charges a stamp duty on this agreement.

- The Cost: It varies by state but is a statutory charge. In some states, this is a nominal fee, while in others, it is a percentage of the loan amount. This is often deducted directly from your loan disbursement amount, reducing the actual cash you receive.

C. Franking Charges

Before the loan agreement or sale agreement is signed, the document must be "franked" (stamped) to make it legal.

- The Cost: This is usually a small percentage of the document value, paid to an authorized bank or agency to stamp the papers.

D. Legal & Technical Verification

The bank does not trust the builder's word or your word. They hire their own lawyer to check the property title chain and an engineer to value the construction quality.

- The Cost: Banks often pass this fee to the buyer. It covers the professional fees of the lawyer and the valuer.

E. Property & Loan Insurance

Banks will aggressively push you to buy "Loan Shield" insurance (to pay off the loan if you die) and Property Insurance (fire/earthquake).

- The Reality: While Property Insurance (which is relatively cheap) is often mandatory to protect the asset, Loan Insurance (which is expensive) is usually optional by central banking rules, though bank agents will claim it is mandatory. Be careful here; you can often get better term insurance separately for a fraction of the cost.

4. The "Moving In" & Third-Party Costs

You have the keys. Now you realize the house is a bare shell. These costs are often ignored until the very last moment.

A. Brokerage

If you used a real estate agent to find the house, their fee is standard and usually non-negotiable in major cities.

- The Cost: Standard market practice is a percentage of the transaction value plus GST. Even if you buy directly from a builder, if an agent facilitated it, they are due their commission (though sometimes the builder pays this). In resale deals, the buyer almost always pays.

B. Interiors & "Bare Shell" Costs

New apartments in India are often handed over with just concrete walls and conduit pipes. There are no lights, no fans, and no cupboards.

- The Basics: You cannot live without fans, tube lights, curtain rods, bathroom mirrors, geysers, and safety grills for balconies (especially if you have kids).

- The Cost: Even for a modest "functional" setup (no fancy decor), the cost of electricals, carpentry, and plumbing fixtures adds up immediately. If you want a modular kitchen and wardrobes, the cost increases exponentially.

C. Relocation Costs

Packers and movers, deep cleaning services for the new house, and pest control before moving in.

- The Cost: Depending on the volume of goods and distance, this is a necessary service that requires immediate cash payment.

5. The Financial Reality Check: A Case Study

To understand the full impact, let us break down the costs for a hypothetical apartment with a Base Price of ₹50 Lakhs. This breakdown illustrates how the "Hidden Costs" stack up to inflate the final budget.

1. The Base Cost: * Agreement Value: ₹50,00,000 * Note: This is the amount your loan eligibility is usually calculated on.

2. The Government's Cut (Payable Out of Pocket): * Stamp Duty (Assumed at approx 6%): + ₹3,00,000 * Registration Charges: + ₹30,000 * GST (5% if Under Construction): + ₹2,50,000 * Subtotal Added: ₹5,80,000

3. Builder & Infra Charges (Often Payable Out of Pocket): * Car Parking (Covered): + ₹2,50,000 * Advance Maintenance (2 Years): + ₹75,000 * Corpus / Sinking Fund: + ₹50,000 * Club House / Utility Charges: + ₹1,50,000 * Subtotal Added: ₹5,25,000

4. Transaction & Loan Costs: * Loan Processing & MODT: + ₹25,000 * Brokerage (1%): + ₹50,000 * Subtotal Added: ₹75,000

5. Making it Livable: * Basic Interiors (Kitchen/Electricals/Grills): + ₹3,00,000 * Subtotal Added: ₹3,00,000

The Final Tally

When you sum up these additional costs (€5.8L + €5.25L + €0.75L + €3L), the total extra expense is ₹14,80,000.

The Real Cost of the Home: The apartment you thought cost ₹50 Lakhs actually costs ₹64.8 Lakhs.

The Cash Flow Crisis: Most importantly, a bank typically funds only 80% of the Base Agreement Value. * Loan Amount: ₹40 Lakhs. * Total Cost: ₹64.8 Lakhs. * Cash You Need: ₹24.8 Lakhs.

You need to arrange nearly 50% of the base property value in liquid cash (savings), even though the "down payment" is theoretically only 20%.

Conclusion: The "20% Buffer" Rule

The excitement of buying a home can quickly turn into anxiety if you run out of cash during the registration process. The smartest way to approach home buying is to follow the 20% Buffer Rule.

Whatever the base price of the property is, calculate 20% of that amount and set it aside purely for statutory taxes, builder fees, and moving costs. This fund should be liquid (savings account or FD), not locked in stocks or mutual funds that fluctuate.

A home is an asset, but buying it is an expense. By accounting for the hidden charges, you ensure that the transaction remains a financial blessing rather than a burden.

Planning your budget? Don't let hidden costs surprise you. Search for properties with transparent pricing on GharPe.

Debojyoti Roy

Creative Content Writer

Debojyoti Roy is a seasoned content‑marketing specialist with 6 + years of digital‑marketing experience. Today, he applies that expertise to a field he loves just as much as careers: helping people find the perfect place to live.

At GharPe.com, India’s first 3‑D/VR real‑estate portal, Roy shapes the entire content strategy and sets the platform’s friendly, trustworthy voice. He creates the foundational guides, checklists and explainer pieces that fuel GharPe’s blog, social‑media feeds and in‑app tips, ensuring every post reflects the site’s signature “see‑before‑you‑buy” approach to property search.

Audience focus

Roy zeroes in on first‑time buyers, young families and anyone curious about the Indian housing market. His plain‑language articles demystify topics like: * understanding 3‑D walkthroughs and drone views * comparing new‑build vs. resale properties * decoding RERA approvals and loan eligibility * negotiating price and spotting hidden costs

Voice of empathy & clarity

Having guided job‑seekers through stressful transitions earlier in his career, Roy writes with the same empathy for house‑hunters. He anticipates their worries (down‑payment deadlines, paperwork jargon, FOMO on better deals, etc.) and answers them in clear, actionable steps that make the buying journey feel manageable.

To make sure this advice reaches everyone who needs it, Roy leans on deep SEO knowledge: keyword mapping for location‑based searches, schema for property listings, and strategic internal‑linking that boosts GharPe’s authority on Google.

Every guide, alert and tip he publishes serves one goal: connecting good people with great homes - fast, confidently and with a little excitement along the way.

Credentials

- Certified Content Marketing Specialist

- Google Analytics Certified

- HubSpot Content Marketing Certified

- SEMrush Content Marketing Toolkit Certified